{kind=link}

July 10, 2025: Vertiv Holdings Co. (VRT Stock Price ) is rapidly cementing its position as a major player in the global AI infrastructure race, driven by booming demand for advanced power and thermal solutions built for high-density compute environments.

In Q1 2025, Vertiv reported a 25% year-over-year increase in backlog to $7.9 billion, while revenue jumped 24.2% YoY to $2.04 billion. The book-to-bill ratio of 1.4x highlights strong and sustained order momentum, especially as hyperscalers and colocation providers expand data center capacity across North America and beyond.

AI Boom Fuels Growth

VRT Stock is leveraging continued R&D investments and manufacturing scale to meet the increasing complexity of AI infrastructure needs. Its strategic collaboration with NVIDIA around GB200 and GB300 reference designs is a pivotal growth catalyst, as AI-native workloads demand robust, integrated infrastructure.

Looking ahead, Vertiv forecasts 2025 revenue between $9.325 billion and $9.575 billion, representing 18% YoY growth at the midpoint, with organic net sales growth of 16.5%-19.5%. Backed by a healthy pipeline and the secular shift toward AI, Vertiv is well-positioned to maintain momentum.

Competitive Landscape Intensifies

However, Vertiv’s dominance is being challenged. Key rivals include:

- Super Micro Computer (SMCI): Advancing liquid-cooled, GPU-optimized systems designed for AI workloads with rapid deployment and energy efficiency.

- Dell Technologies (DELL): Enhancing its AI-ready, integrated infrastructure solutions to support large-scale cloud and enterprise deployments.

Both companies are competing for the same enterprise and hyperscaler market share that Vertiv is targeting.

Stock Performance, Valuation & Estimates

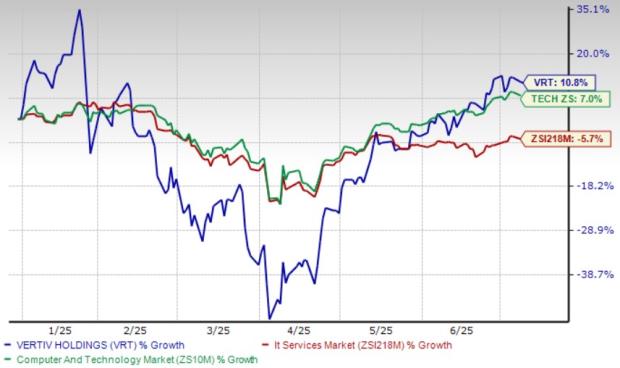

- VRT Stock Price is up 10.8% year to date, outperforming the Zacks Computer & Tech sector (+7%) and the IT Services industry (-5.7%).

- VRT Stock Price trades at a Price/Book ratio of 17.99x, significantly higher than the sector average of 10.2x, reflecting investor confidence but also a rich valuation.

- It holds a Zacks Rank #2 (Buy) with 2025 earnings projected at $3.56 per share, marking a 24.91% increase YoY.

Despite a Value Score of D, the company’s forward momentum and AI tailwinds continue to drive bullish sentiment.